Mortgage Blogs

Stay up to date with the recent industry news and mortgage trends.

Toronto Mortgage Broker Insights: 3 Smart Ways Income Changes Can Shape Your Mortgage

Toronto Mortgage Broker Guide for Homeowners Facing Income Changes

Life does not stay the same for five years, but your mortgage often does. Many homeowners are surprised to learn that changes in income usually do not affect their existing mortgage right away. As long as payments are made on time, lenders rarely reassess your financial situation during the term.

However, income changes can matter later. As a professional Toronto mortgage broker, I often speak with current homeowners who are unsure how job changes, self-employment, or reduced hours may affect future mortgage plans. Understanding how renewal, refinancing, and long-term planning work can help you stay confident and prepared.

Below are three key things every homeowner should keep in mind.

Why Mortgages Stay the Same While Life Changes

Understanding Fixed Mortgage Terms

Most mortgages are set for a specific term, commonly three to five years. During this period, the lender bases your approval on your income, credit, and debt at the time you applied. Once the mortgage is funded, those details usually stay locked in until the term ends.

This means that if your income goes up or down during the term, it does not automatically change your mortgage payment or conditions.

Common Income Changes Homeowners Experience

Homeowners often experience income changes such as:

Career moves or promotions

Transitioning to self-employment

Reduced hours or temporary layoffs

Parental leave or retirement planning

While these shifts may not affect your mortgage immediately, they can influence your next steps.

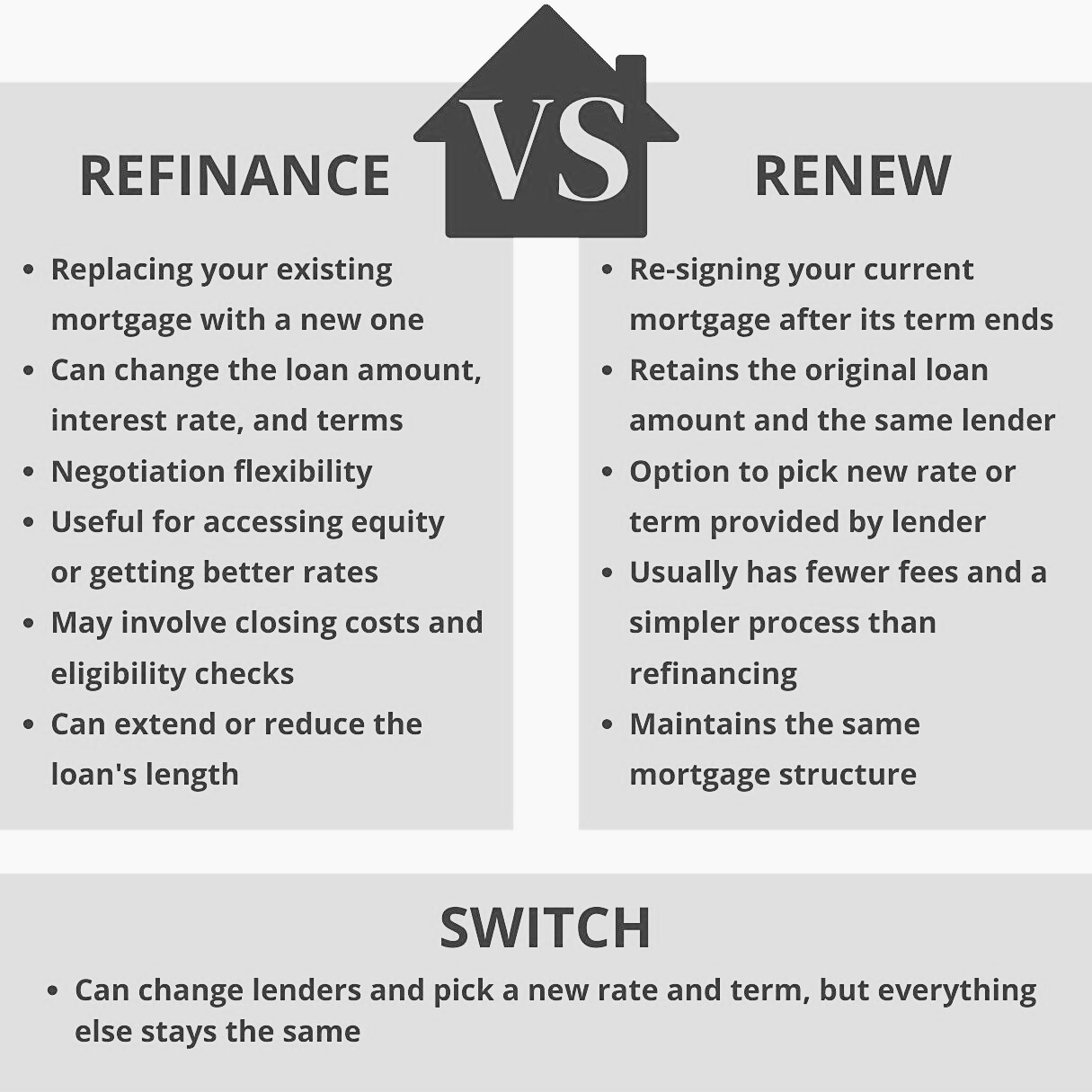

First Key Point: Renewal Is When Income Matters Again

Mortgage renewal is often when income becomes important once more.

What Lenders Review at Renewal

If you stay with your current lender and simply renew, the process is usually straightforward. In many cases, no income verification is required. However, if you want to switch lenders, adjust your mortgage, or negotiate better terms, your income may be reviewed again.

How Income Changes Can Affect Your Options

If your income has decreased, your options may be more limited. On the other hand, a higher or more stable income could open doors to better rates or different products. A Toronto mortgage broker can help you understand whether staying put or exploring alternatives makes sense based on your current situation.

Second Key Point: Refinancing Looks at Your Current Situation

Refinancing is different from renewal and almost always involves a full financial review.

What Triggers Refinancing Decisions

Homeowners refinance for many reasons, including:

Accessing home equity

Consolidating debt

Funding renovations

Adjusting mortgage terms

When refinancing, lenders assess your present income, debts, and credit profile.

Income, Debt, and Home Equity Explained

Even if your home value has increased, income still matters. Lenders want to ensure you can manage the new payment comfortably. If your income has changed, refinancing may still be possible, but structure and timing become very important.

Third Key Point: Planning Ahead Gives You More Options

The earlier you plan, the more flexibility you tend to have.

Why Early Planning Reduces Stress

Waiting until the last minute can limit your choices. By reviewing your mortgage well before renewal or refinancing, you can identify potential challenges and address them early.

Strategies to Prepare for Income Changes

Planning may include:

Reviewing your mortgage one to two years before renewal

Reducing other debts

Building savings as a buffer

Exploring alternative mortgage options

A proactive approach can make a meaningful difference.

How a Toronto Mortgage Broker Supports Homeowners

Advice Beyond Interest Rates

A Toronto mortgage broker does more than shop for rates. The real value lies in understanding your full financial picture and how future income changes may affect your goals.

Customized Mortgage Planning

Every homeowner’s situation is different. Whether income is increasing, decreasing, or becoming less predictable, personalized planning helps you stay prepared rather than reactive.

Common Mistakes Homeowners Make

Some of the most common mistakes include:

Assuming income changes do not matter at all

Waiting until renewal to seek advice

Refinancing without understanding long-term costs

Not planning for future flexibility

Avoiding these missteps can save time, stress, and money.

Frequently Asked Questions

Does a drop in income affect my current mortgage?

Usually no, as long as payments are made on time during the term.

Will my lender check income at renewal?

Often not if you stay with the same lender, but switching lenders may require verification.

Can I refinance with lower income?

Yes, but approval depends on your overall financial profile, including debt and equity.

Is it better to plan early if my income might change?

Yes. Early planning provides more options and less pressure.

Can a mortgage broker help even if I am not renewing yet?

Absolutely. Early advice helps you prepare strategically.

Who should I talk to if I am unsure about my options?

A Toronto mortgage broker can review your situation and explain choices clearly.

Conclusion and Next Steps

Life changes, and income changes are a normal part of that journey. While your mortgage may not react right away, renewal and refinancing are moments when your current situation matters again. Planning ahead gives you more control and more options.

If your income is changing and you are unsure how it affects your mortgage plans, I am happy to talk it through and help you plan with confidence.

Trusted Guidance, Proven Success

Alan Borcic | Mortgage Strategist

(647) 694-7033

Assistance Hours

Mon – Fri 9:00am – 8:00pm

Saturday/Sunday – CLOSED

Get In Touch With

(647) 694-7033

Assistance Hours

Mon – Fri 9:00am – 8:00pm

Saturday/Sunday – CLOSED

Contact Us

© 2026 Mortgage With Alan - All Rights Reserved.

Alan Borcic, Mortgage Strategist M24001034

BRX 13463