Mortgage Blogs

Stay up to date with the recent industry news and mortgage trends.

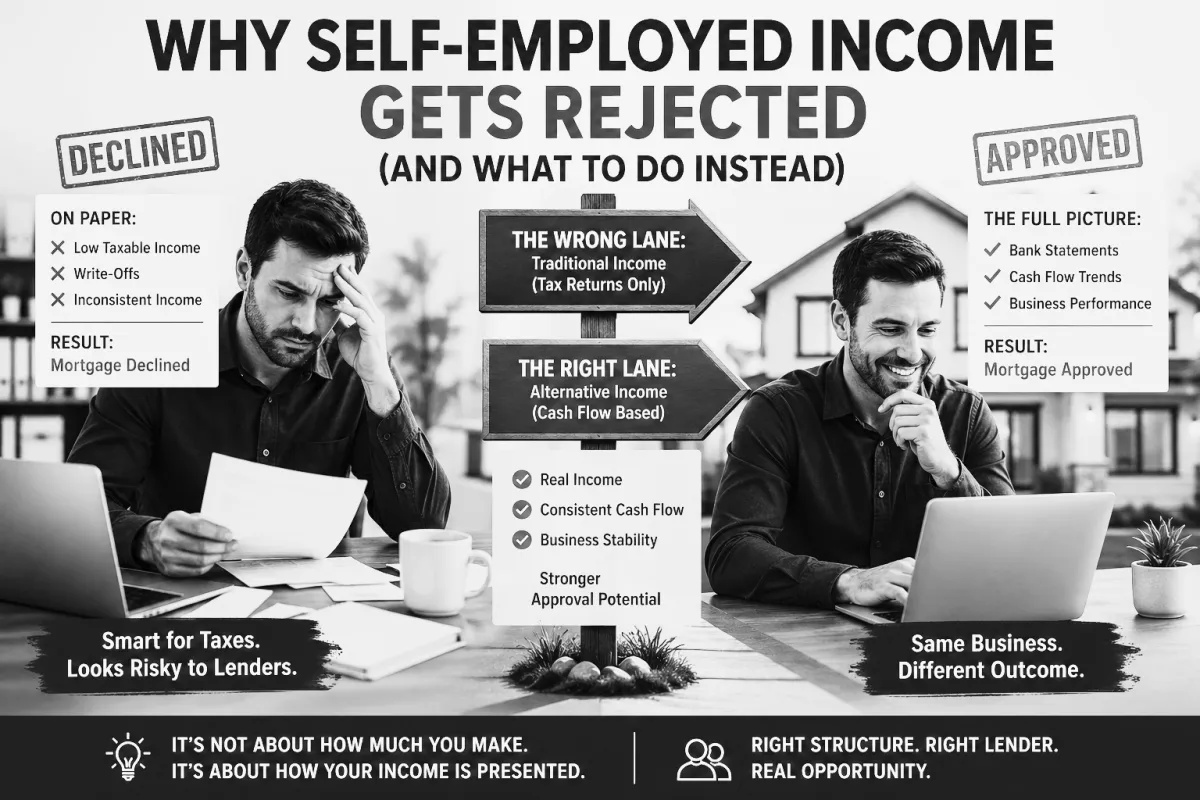

Why Self-Employed Income Gets Rejected (And What To Do Instead)

You can run a profitable business…

and still get declined for a mortgage.

That’s not a contradiction.

It’s how the system is built.

The Real Problem: You Look “Bad” on Paper

Most self-employed business owners do two things well:

Generate revenue

Reduce taxes

The problem?

Those two goals conflict when it comes to mortgages.

You write things off.

You manage your income.

You keep your tax bill low.

Smart business move.

But when a lender looks at your file?

They don’t see strategy.

They see low income.

Banks Don’t Understand How You Get Paid

Traditional lenders are built for one type of borrower:

T4 employees with stable, predictable income

Same paycheck. Every month. Easy to verify.

But self-employed income?

It fluctuates.

It’s structured.

It doesn’t follow a straight line.

So instead of trying to understand it…

Banks default to what’s easy:

Your tax returns (T1 Generals)

Your Notice of Assessment

If those numbers look low?

You’re out.

The “On Paper vs Reality” Gap

Here’s what this looks like in real life:

You make $120K+ in your business

But after write-offs… you show $55K

To you → you’re doing well

To the bank → you’re borderline unqualified

That gap is where most deals die.

Not because you can’t afford the home…

But because your income doesn’t translate cleanly on paper.

What Lenders Actually Care About

Here’s the part most people miss:

Lenders aren’t asking:

“Are you making a lot of money?”

They’re asking:

Is this income real?

Is it consistent?

Is it likely to continue?

That’s it.

And there’s more than one way to answer those questions.

The Two Paths Most People Don’t Know About

1. Traditional Income (A Lender Route)

If your tax returns show strong, consistent income over 2 years:

• You’ll qualify with major banks

• You’ll get the best rates

• Minimal friction

This is the cleanest path.

But it doesn’t work for everyone.

2. Alternative / Stated Income (B Lender Route)

If your income looks low on paper, but your business is strong:

There’s another way.

Instead of relying only on tax returns, lenders can look at:

• Business bank statements

• Cash flow trends

• Revenue consistency

This gives a more accurate picture of what you actually earn.

Yes, this route may come with:

• Slightly higher rates

• Larger down payment (often 20%)

But it gets deals done that banks would decline.

Why Most People Get Declined

It usually comes down to one thing:

They’re trying to force the deal through the wrong lane

Bank says no → they assume they’re unqualified

In reality?

They just needed a different approach.

Same business.

Same numbers.

Different outcome.

What To Do Instead

If you’re self-employed and thinking about buying:

Stop asking:

“Will the bank approve me?”

Start asking:

“What’s the right way to structure my income for this?”

Because approval isn’t just about income.

It’s about how that income is presented and interpreted.

The Bottom Line

Being self-employed doesn’t make you a risky borrower.

It just makes you a different one.

And if you’re being evaluated like a T4 employee…

You’re going to get the wrong answer.

If your income doesn’t tell the full story on paper,

it’s worth getting a second look before assuming you don’t qualify.

I’m happy to walk through your situation and point you in the right direction.

Trusted Guidance, Proven Success

Get Mortgage Answers Before You Make Expensive Financial Decisions

Alan Borcic | Mortgage Strategist

(647) 694-7033

Assistance Hours

Mon – Fri 9:00am – 8:00pm

Saturday/Sunday – CLOSED

Get In Touch With

(647) 694-7033

Assistance Hours

Mon – Fri 9:00am – 8:00pm

Saturday/Sunday – CLOSED

Contact Us

© 2026 Mortgage With Alan - All Rights Reserved.

Alan Borcic, Mortgage Strategist M24001034

BRX 13463