Mortgage Blogs

Stay up to date with the recent industry news and mortgage trends.

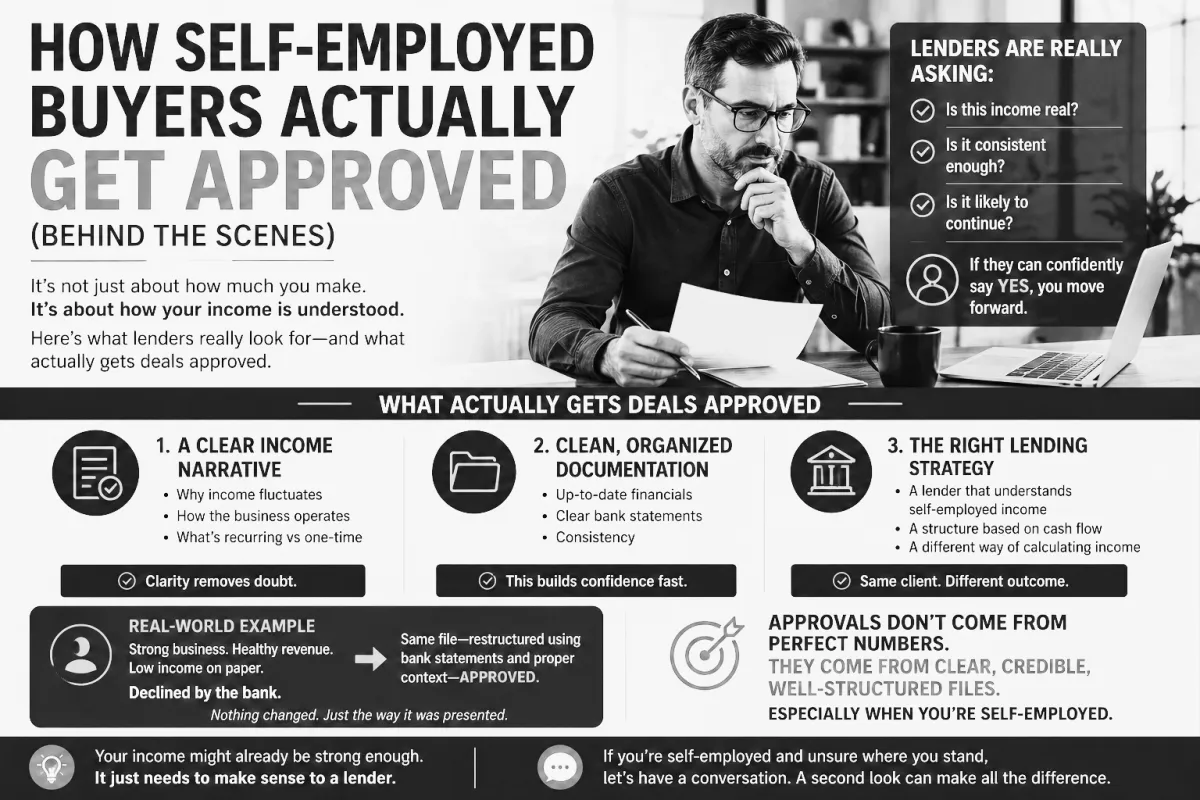

How Self-Employed Buyers Actually Get Approved (Behind the Scenes)

Most people think mortgage approvals come down to one thing:

Income.

That’s only half the story.

Because you can have strong income…

and still get declined.

The Real Game: It’s Not Income, It’s Interpretation

Lenders don’t just look at numbers.

They interpret them.

And for self-employed buyers, that’s where things break.

Because your income isn’t simple:

It fluctuates

It’s optimized for taxes

It doesn’t follow a clean pattern

So when it’s presented poorly?

It creates one thing:

Doubt

And doubt kills approvals.

What Lenders Are Actually Trying to Figure Out

Forget what you’ve heard about “high income.”

Lenders are really asking:

Is this income real?

Is it consistent enough?

Is it likely to continue?

If they can confidently answer “yes”

Deals get approved.

If not?

They pass.

Why Strong Buyers Still Get Declined

Here’s what usually goes wrong:

1. The Income Doesn’t Tell a Clear Story

Numbers don’t line up

Fluctuations aren’t explained

No context is provided

From the lender’s perspective?

It feels risky

2. The File Is Messy

Missing documents

Inconsistent reporting

Unclear structure

Even a good income looks weak when it’s disorganized.

3. The Wrong Approach Is Used

Everything gets forced through:

Tax returns only

One lender

One method

When that doesn’t fit?

The deal dies.

What Actually Gets Deals Approved

Now the important part.

Here’s what works behind the scenes:

1. A Clear Income Narrative

Not just numbers, context.

Why income fluctuates

How the business operates

What’s recurring vs one-time

This removes doubt.

2. Clean, Organized Documentation

Simple wins here.

Up-to-date financials

Clear bank statements

Consistent reporting

This builds confidence.

3. The Right Lending Path

Not every deal belongs with a traditional bank.

Sometimes it’s:

A lender that understands business income

A structure that reflects real cash flow

A different way of calculating income

Same client.

Different lens.

The Shift Most People Need to Make

Stop thinking:

“Do I make enough?”

Start thinking:

“Does my income make sense to a lender?”

Because those are two very different things.

Real-World Example (Simplified)

Self-employed client:

Strong revenue

Healthy business

Low income on paper

Declined at the bank.

Same file, restructured using bank statements and proper context

Approved.

Nothing changed.

Just how it was presented.

The Bottom Line

Approvals don’t come from perfect numbers.

They come from:

Clear, credible, well-structured files

Especially when you’re self-employed.

If your income is solid but hard to explain on paper,

It’s worth getting a second look before applying.

A small change in how it’s presented can make a big difference.

Trusted Guidance, Proven Success

Get Mortgage Answers Before You Make Expensive Financial Decisions

Alan Borcic | Mortgage Strategist

(647) 694-7033

Assistance Hours

Mon – Fri 9:00am – 8:00pm

Saturday/Sunday – CLOSED

Get In Touch With

(647) 694-7033

Assistance Hours

Mon – Fri 9:00am – 8:00pm

Saturday/Sunday – CLOSED

Contact Us

© 2026 Mortgage With Alan - All Rights Reserved.

Alan Borcic, Mortgage Strategist M24001034

BRX 13463